Are you a Deakin student struggling with debt? You have options.

Having some debt isn't bad if it's kept under control, but it can be tough keeping up with repayments on a student budget. If you're struggling with consumer credit debt like BNPL, credit cards, or personal loans, seek help quickly. Don’t ignore your debt!

This page outlines the steps to take if you are struggling to make your Australian credit repayments, as well as more information specific to the different types of credit products, and some alternatives to using credit while you're a student.

This information is provided by DUSA Financial Wellbeing. Visit the DUSA Financial Wellbeing webpage for more information about this service.

Steps to take if you are struggling with consumer credit repayments

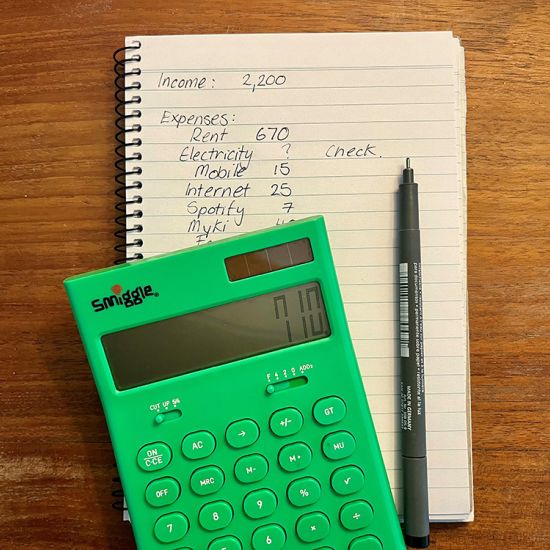

1. Work out what you can afford to pay

- Create a simple budget by adding up all your income and all your expenses. The MoneySmart budget planner is a useful tool to work this out.

- Review your expenses. First, separate your costs into ‘needs’ and ‘wants’. What are the things you can’t do without (such as food or rent)? These are your ‘needs’. What are the things that you could do without (such as Netflix or takeaway coffee every morning)? These are your ‘wants’. Are there any expenses that you can cut? Be realistic.

- Subtract your money going out from money coming in. The MoneySmart budget planner will automatically do this for you. The amount left over is how much you can pay towards your debt. If this is less than your required repayments, then move on to Step 2.

- It is important to know how much you can afford to pay before you speak to your provider and agree to any payment plan.

2. Contact your provider to let them know you are having trouble paying

- Most providers have financial hardship teams who are trained to support you. Ask to speak to the ‘hardship department’. You can check your provider’s website for how to contact them to discuss hardship. Options may include calling, emailing or completing a form on their website.

- When you contact your provider, ensure that you have your account details available.

- Tell your provider that you are experiencing financial hardship and cannot make your repayment. Let them know how much you can afford to pay.

- Your provider may ask for details about your situation and what has led to your financial hardship. You can share as much as you feel comfortable with.

- The provider needs to give you information about your options such as a payment plan with reduced payments or taking a break from payments for a period of time.

- See below for information specific to buy now pay later, credit card, and personal loan debt.

3. Request confirmation of any new payment arrangement in writing.

Keep this confirmation for your own records, and as a reminder of the arrangement.

4. If you think you have been treated unfairly you can make a complaint

You can make a complaint to the provider and if you are still unsatisfied you can make a complaint to AFCA, the external dispute authority.

Disclaimer